The economic crisis that accompanies the COVID19 break and its health crisis has generated stock market crashes that had never been seen before. Steeper and deeper than the 1929-31 decline, the stock market crashes pushed the panic button of the Central Banks of advanced economies. Terrified of a total collapse of all securities that would generate problems of banking and financial failures, they came to the rescue. The immediate solution was to inject 3 trillion dollars of credit into the system in the United States. This was replicated by the ECB and the Bank of England. The idea was to induce the banks to put that money into the stock markets and thus stabilize them.

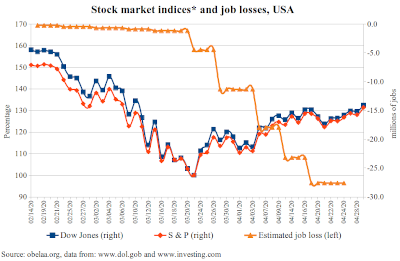

In the United States, between February 25 and March 23rd, the financial markets had lost more than 30% of the value of their assets and the outlook was worse. On March 23rd the Fed announced a new measure of more than one trillion dollars, thus accumulating an injection of more than 3 trillion. With this it managed to stop the fall of the financial market, (see the graph) and record the best performance of its stock markets since 1938. On the contrary, the U.S. economy has accumulated, since February 2020, more than 27 million jobs lost, the highest in its history. Then, in an antithetical and irrational way, the economy that has projected to lose -5.9% of its GDP and increasing unemployment has a stock market recovery.

According to the latest issue of the International Monetary Fund's World Economic Outlook, published in April, the impact of COVID19 on the world economy will be a contraction of -3% in economic growth. A fall of -6.1% was estimated for advanced economies, with stronger contractions in Italy, -9.1%; Spain, -8%; France -7.2%; Germany, -7.0%; and the United Kingdom, -6.5%. Latin America and the Caribbean are estimated to contract by -5.2%, with harder effects in Mexico -6.6%; Ecuador -6.3%; Argentina -5.7%; and Brazil -5.3%. Overall, as many have already acknowledged, this is the biggest crisis in the history of capitalism.

In any case, although most of the measures to create monetary liquidity have been aimed at sustaining financial returns, they do have an impact on the real economy, although not in the same proportion, insofar as they are aimed at refinancing the debts of closed businesses or those with fallen sales. In addition, there is increased fiscal spending, including direct transfers of income to households and, in exemplary cases such as Chile and Spain, the building of a guaranteed universal minimum living income. This guarantees access to livelihoods for the population, allows for the adoption of distancing measures and promotes the reactivation of the domestic market. The pending issue is the promotion of real investment and production.

However, not all economies have this fiscal, monetary and financial capacity to implement such measures. COVID19 has also expressed all the asymmetries existing between developed countries and those with lower levels of development. More than thirty years of decreasing State participation, privatization of public services and, for that matter, the abandonment of free health systems, caused immense difficulty in the capacity to contain this and any health crisis.

The globalization of production and trade tended towards countries with lower labour costs and fiscal preferences. This logic implied that the condition of work in these countries has been developed on informality and the disappearance of labour rights: unemployment insurance, work disability, retirement savings, social security, medical services. Under these conditions there are no labour guarantees, universal unemployment insurance, paid social benefits, etc. In Latin America, for example, more than 53% of workers are in the informal sector, and about 38% of the population lives below the poverty line and 11% in extreme poverty. This is why social distancing and unemployment measures are so difficult to implement and sustain for long periods. That is also why universal unemployment insurance is so urgent.

The question of the instantaneous rescue of the stock market and the financial sector on March 23 with the injection of $3 trillion when unemployment rises raises the question of the importance of the financial sector for decision-makers and policy makers. Conversely, it speaks to the second place of universal income insurance and income redistribution mechanisms that could assist in the recovery of aggregate demand in these bleak times.

Download