After 2018 and 2019, difficult years due to the US trade war with China, Britain's separation from the European Union and the fall in US growth rate while the stock markets rose, 2020 broke all expectations.

The most spectacular fall in global economic growth in history showed that, while Asia fell little, Europe and Latin America fell a lot and the US fell a little less than Europe, but much more than Asia. China rebounded in the second quarter of 2020, as the rest of the world entered the depths of the fall, and ended the year with positive economic growth.

The rebound in the third quarter has been remarkable. The depth of the decline was related to the speed of growth prior to the fall. The more growth, the less the fall. The exception was Peru. High growth and deep fall. The rebound is symmetric and the bigger the fall, the greater the initial rebound. Thus, the data for the second half of the year were positive, prompting some to say the crisis was over.

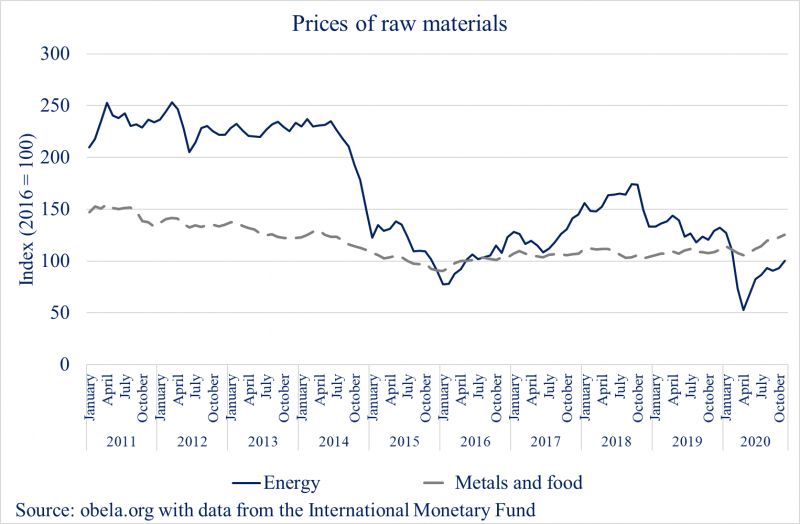

The crisis is not over neither in terms of health nor the economy. The magnitude of a crisis is appreciated not during the fall but when it hits the bottom. It is like a person falling off a building that while falling is alive. The critical point is when the person hits the ground. When economic activities are reopened, then the problems of lack of demand, business debt and unemployment are appreciated. Supply wise the problems of production and distribution are also foreseeable. From the point of view of international trade, surprisingly, commodity prices recovered except for fossil fuels. The reason for this was not a reactivation of demand, because global demand is considerably lower than in 2019, but rather the injection of 3.5 billion dollars (15% of US GDP) into the investment banks and hedge funds that refloated the stock and commodity markets from 23 March of this year. All commodity price curves changed course that day except for fossil fuels. Private investment, which was already affected earlier, remains affected. With negative interest rates in the US and the EU, hedge funds borrow and invest on the stock market. This explains the disconnection between stock market indices and US GDP growth rate, in what is clearly a speculative bubble.

While the US economy had been on a downward path of growth since March of 2018, in 2020 it plummeted to -32% per year in the second half of 2020, levels never seen before. Faced with such a fall, the Federal Reserve, in its first monetary policy decision of the year, lowered the federal bond benchmark rate in the range of 0.25- 0.50% due to the economic slowdown, leading to a round of central bank rate cuts worldwide. This generated arbitrage opportunity towards emerging countries with an impact on the exchange rate against other currencies, increases in international reserve levels and a strengthening of Latin American exchange rates in general.

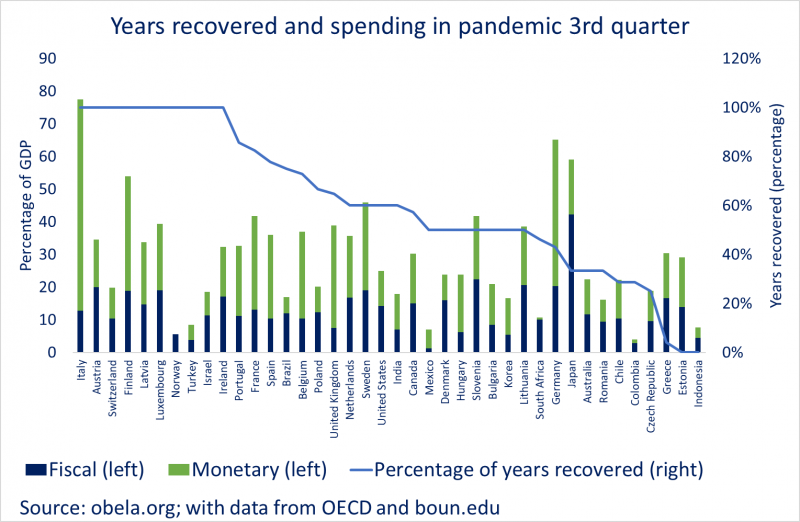

International trade is recovering rapidly, contrary to July's estimates, bringing initial rebounds to very high levels. The problems are more fiscal than external. The slumps in GDP are accompanied by falls in tax revenues, which make it difficult to maintain stable spending levels. The Mexican solution has been to cut spending in an orthodox manner. Others Latin American countries preferred to increase domestic debt.

There is a mirage in progress. The collapse of GDP for all, together with the stability of the external debt, has resulted in rising debt-to-GDP ratios and the image of an increased foreign debt problem. However, if reserves increase, there are no external debt problems. On the other hand, falling tax revenues at a time of rising public spending on health leads to more domestic debt, and this leads to fiscal, not debt, problems. The new debt is with social security and pension funds intermediated by private banks within countries.

Finally, we reiterate what we wrote a year ago, the general trend of the world economy is expected to continue its slow pace in most economies, with the clear contrast of the Asian economies which will continue to grow swiftly. This dynamic will change the economic axes from the Atlantic to the Pacific in a stable manner from now on in spite of. Asia being particularly affected by the protests in Hong Kong and India. For the advanced economies the prognosis is grey, because the EU's problems do not end with the UK's departure Poland could be a candidate for a Polxit given the EU's criticism of its nationalist policies and Hungary (Hunxit) remains to be seen. On the other hand, Central and South America are facing rather complicated situations on several fronts, with political instability and open interference by the United States. There are active youth social movements in the countries on the Pacific coast, and it remains to be seen whether they will expand to those on the Atlantic coast, Brazil and Uruguay in particular. Together with Africa, it will be one of the areas that will grow the least this year and next. The star country, Bolivia, has returned to democratic status and it remains to be seen how Ecuador, Colombia and Venezuela will manage to grow with depressed fossil fuel prices that have no return. Mexico exports petrol fueled cars to a market that buys fewer cars while it has been left with a huge empty tourist infrastructure, along with the Caribbean islands and Peru. It is estimated that by 2024 the world will return to pre-pandemic levels. When that happens, it will be with another energy matrix and other external actors in the region.